Historically, data about our financial lives has been stored separately, and siloed, within the walls of traditional institutions. For this reason, until now, our understanding of financial information has been limited almost exclusively to banking services.

But what would happen if we broke down these walls to make financial information accessible through new channels? What if the real owners of this information were the users and they could choose when and how to share it with a company?

This is precisely what Open Banking is all about: allowing individuals to share their financial information with third parties through application programming interfaces (or APIs).

Opening up new channels to understand people’s finances

One of the first examples of Open Banking implementation took place in the UK in 2016, when the country issued a rule that required the nine biggest banks in the country to allow licensed startups direct access to their data through standardized APIs. For the first time, millions of customers had the chance to share their banking information with new companies –like fintechs, and neobanks–that started leveraging these new sources of data to provide them with new solutions tailored to their real needs.

Since then, a lot has happened.

New digital players are flourishing worldwide, and similar regulations have also been introduced in other regions like Europe, Australia, and the US, creating new ways to share financial data. Now, these models are evolving quickly in Latin America.

From Open Banking to Open Finance

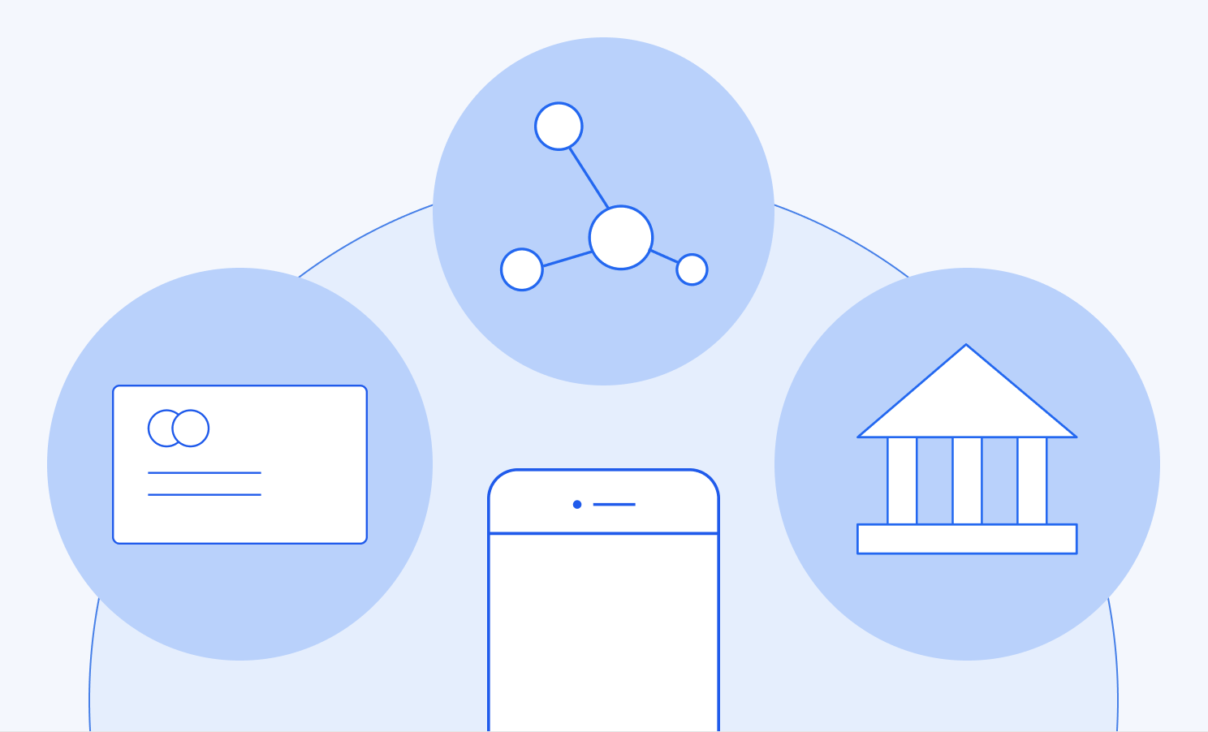

One of the more revolutionary characteristics of this new type of information exchange is that it can work in many directions: whether that is users sharing the information they store in their banking accounts with new digital platforms or the other way around. And that it is not necessarily limited to banking data. This is known as Open Finance: a step beyond Open Banking where financial data –no matter where it comes from–, can be shared with multiple parties to foster the development of new products and services.

This includes financial data from digital players like big tech companies, fintechs, or gig economy platforms, as well as traditional entities like fiscal institutions, payroll service providers, insurance issuers, retailers, or even utility providers like electricity companies.

Wherever bills are being paid, and money is changing hands, there’s data that can help describe people’s real financial lives.

These characteristics make Open Finance an ideal model for Latin America, where in some countries up to 50 percent of the population does not have a bank account with a traditional institution.

However, people in Latin America are increasingly using other channels on a daily basis to carry out the transactions they need. And this data can help expand their eligibility for new products and services.

More inclusive services and products

Thanks to these new API-based communication channels, data from these alternative sources can also move freely, when users choose to, across the different apps and platforms that they use in their daily lives, for shopping, paying bills, receiving money from their families and friends, working, or taking care of other financial transactions.

And by having new ways to access it, new digital players can use it to create new products and services around it and provide users with a better understanding of their financial situation.

Through these same roads, financial information can also be enriched using data science and machine learning so that companies can extract its value and turn it into more relevant and tailored services for their customers. Having these new ways of connecting financial institutions thanks to APIs can also enable new services, like making instant bank-to-bank payments and other transactions more easily, inside the apps themselves.

By allowing financial information from a wider range of sources to easily and securely flow between different apps and digital solutions that people use in their daily lives to manage their finances, it is possible to create a more inclusive financial system. One where users can access the services they truly need, in a safe way, and with the freedom to choose from a wider range of possibilities. This, in turn, generates greater competition in financial services, fosters more innovation, and results in greater well-being for millions of people.

This secular movement is very much underway and is very aligned with our mission at Belvo to power the next generation of financial services in Latin America through a bank and financial data APIs platform.

And to understand what awaits in the near future, we prepared this report to uncover and share some of the key trends to expect within Open Finance this year.